What a Landscaper at One of My Open Houses Taught Me About Who's Ready to Invest

Shaaron Honeycutt May 4, 2026

Shaaron Honeycutt May 4, 2026

A few Saturdays ago I was hosting an open house at one of my listings in the Estrella at Sunstone community in Northwest Las Vegas. A landscaper showed up to give the homeowner a quote on the yard — the HOA had nudged her to get it cleaned up before the listing went live.

We got to talking on the front lawn, and somewhere between shrub trimming and curb appeal, the conversation turned to real estate investing. He had been thinking about it for a while. He owned his own business, worked hard, and had some money set aside. But he assumed that because his tax returns didn't tell the full story of what he actually earned, a traditional mortgage would be tough to qualify for.

He was right about traditional loans. But he hadn't heard of a DSCR loan.

I told him he might be a natural fit. And I thought: if he didn't know, there are probably a lot of other hardworking, self-employed people in Las Vegas who don't know either.

So here's the introduction I wish more people had.

DSCR stands for Debt Service Coverage Ratio. It sounds technical, but the idea is simple.

A DSCR loan qualifies you based on what the property earns, not what you earn. There are no W-2s required. No tax returns. No explaining away business write-offs to an underwriter.

The lender asks one core question: does the rental income cover the mortgage payment?

Here's how the ratio is calculated:

Monthly Rental Income divided by Monthly Debt Service (principal, interest, taxes, and insurance)

A ratio of 1.0 means rent exactly covers the payment. Most lenders want to see 1.20 or higher, meaning the property brings in at least 20% more than it costs to carry. Some lenders will go as low as 1.0 for well-qualified borrowers.

For self-employed business owners whose income looks complicated on paper, this is a genuine advantage.

Before you make an offer on any investment property, run through this simple framework.

If the property already has a tenant, use the current lease amount. If it's vacant, research comparable rentals in the same neighborhood to estimate market rent. A property that already has a lease in place is generally easier to finance and analyze since there's no guesswork involved.

This is where a lot of new investors underestimate costs. Factor in all of the following:

Subtract your operating expenses from gross rental income. What remains is your NOI. This is the number that feeds your DSCR calculation, and it's the truest picture of what a property actually produces.

Once you subtract the mortgage payment from your NOI, what's left is your monthly cash flow. A healthy margin on a single-family rental in the Las Vegas market is generally $200 to $400 per month at minimum. More is always better, but that range is a reasonable starting benchmark.

If you want to go deeper before your first conversation with a lender or agent, here are three resources I genuinely recommend:

BiggerPockets (biggerpockets.com) — The go-to community and learning platform for rental property investors. Their calculators, forums, and beginner guides are outstanding. Their YouTube channel is excellent too.

Investopedia on DSCR Loans (investopedia.com/terms/d/dscr.asp) — A clear, jargon-free explanation of how the ratio works and what lenders look for.

Michael Zuber, "One Rental at a Time" (YouTube) — He walks through real deals with real numbers. If you're a visual learner, start here.

If you're self-employed, own a business, or simply feel like a traditional mortgage isn't your best path into real estate investing, a DSCR loan may be worth a conversation.

Here's how I can help:

I work with a trusted group of lenders here in Las Vegas who specialize in investor financing, including DSCR loans. I'm happy to connect you with the right person to talk through the financial side of things. That's always a great place to start.

Once you have a sense of what you can qualify for, I can help with the property search. I specialize in Northwest Las Vegas, Summerlin, and the surrounding communities, and I know the rental market well.

Reach out anytime. You can call or text me at 702.556.8121, email me at [email protected], or simply visit honeyimhomeLV.com to learn more.

There's no pressure and no commitment. Just a conversation — kind of like the one that started on a front lawn in Sunstone.

Shaaron Honeycutt | REAL Broker LLC | NV S.190721 Serving Northwest Las Vegas, Summerlin, North Las Vegas, and surrounding communities 702.556.8121 | [email protected] | honeyimhomeLV.com

Weekly Las Vegas Market Report — July 21, 2026

Here's What The Numbers Say...

The Nine Ds of Real Estate

Las Vegas Real Estate Market Report — May 2026 By Shaaron Honeycutt | REAL Broker LLC

By Shaaron Honeycutt | REAL Broker LLC | Las Vegas Real Estate

From Boutique to Franchise to... Wait, THIS Is What I Was Looking For

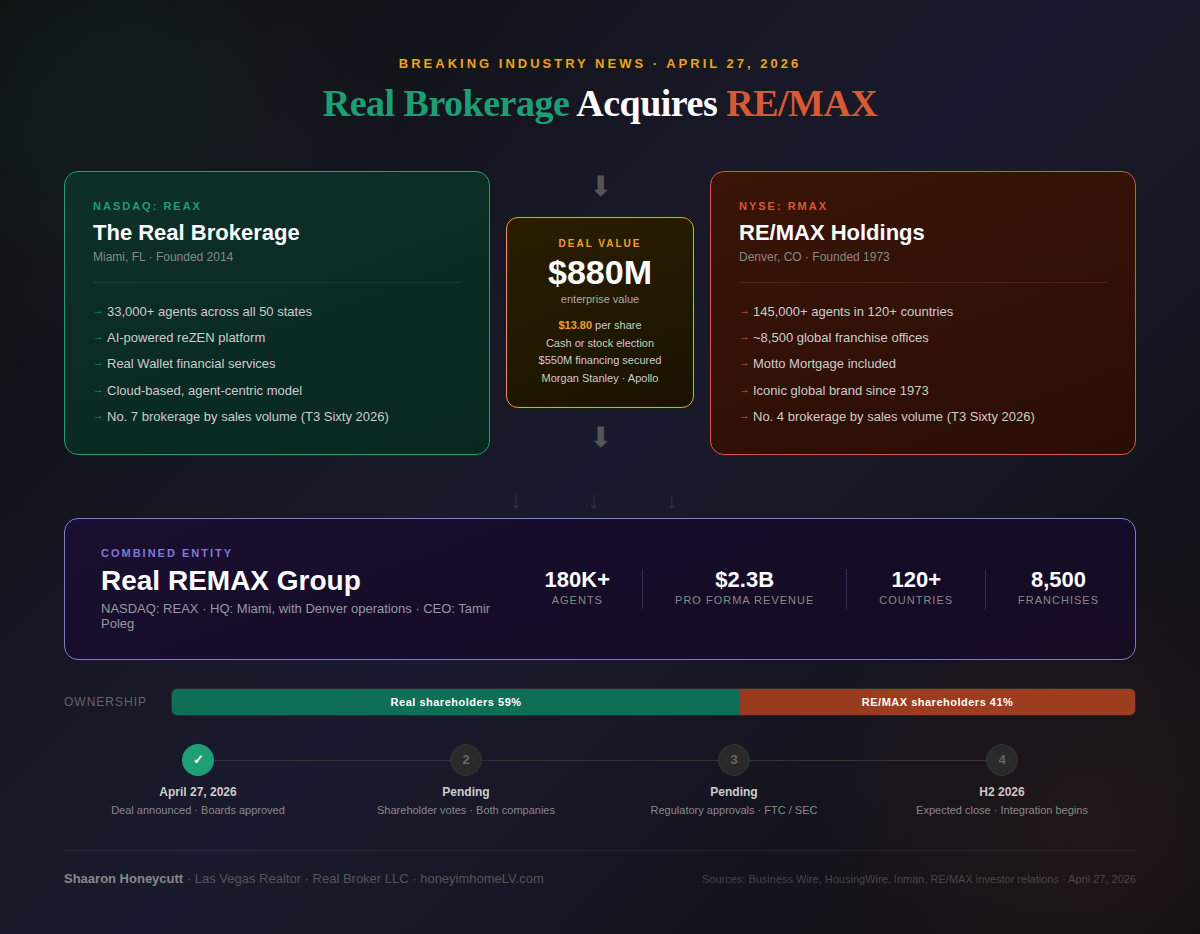

The biggest news in real estate right now isn't about interest rates or inventory. It's a deal that's reshaping who controls the industry.

Don't Trust Zillow to Price Your Home. Here's Why.

When you work with Shaaron, you’re not getting someone who dabbles in real estate. You’re getting a full-time, full-heart advocate who’s committed to excellence, strategy, and serving people well before, during, and long after the deal closes.

7997 W SAHARA AVE #101 LAS VEGAS NV 89117